‘Tenant’s playground’: office vacancy at 30-year high

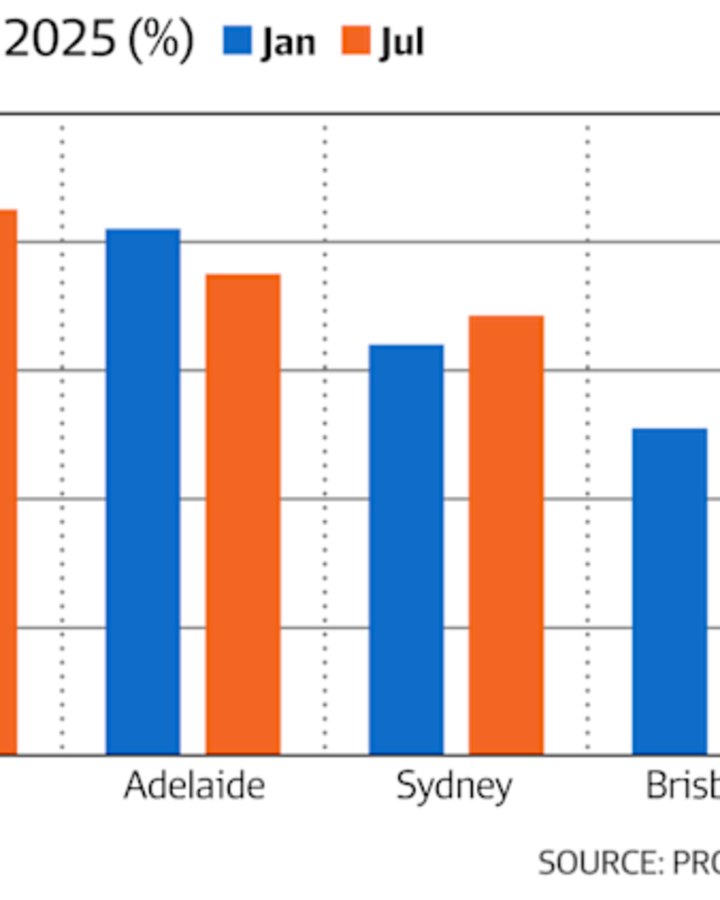

The vacancy rate across Australia’s office markets has risen to 15.2 per cent nationally, its highest in around three decades, as new supply hits the market faster than it can be taken up.

The Property Council of Australia, which compiles the six-monthly updates, says that it is because of a broader shift to better quality space, with a raft of CBD landmarks being built to accommodate that demand.

As new supply rose, the national CBD vacancy rate edged higher to 14.3 per cent in the six months to July. Suburban vacancy held virtually steady at 17.3 per cent. Over 200,000 square metres of supply has been added to the national market in the past six months, outstripping demand for space.

Property Council chief executive Mike Zorbas said the slew of new office supply over the past few years is part of “a refresh of office spaces” as tenants demand higher quality spaces.

“The continuous supply of new high-quality office space in our CBDs is a response to businesses searching out great places for their employees to work in,” he said.

“Tenants are capitalising on opportunities to occupy premium buildings in prime CBD locations, with premium space continuing to see higher demand levels than lower-grade buildings.”

Melbourne has the nation’s emptiest CBD offices, with a vacancy rate of 17.9 per cent, down only fractionally compared to six months ago. Perth is at 17 per cent and Sydney’s CBD edged higher to 13.7 per cent.

Outside the CBDs, the vacancy rate is highest in Sydney’s Crows Nest and St Leonards, is around 30 per cent.

The latest figures will underscore business worries that Victorian Premier Jacinta Allan’s commitment to legislate working from home rights of at least two days a week will put further pressure on the Melbourne CBD’s recovery.

More broadly, the PCA figures show that much of the demand is centred on premium and A-grade buildings, while B, C and D grade office buildings are suffering.

Over the second quarter, around two-thirds of space leased nationally was for premium or A-grade assets, a reflection of tenants’ preference for high-quality spaces in core locations, according to separate analysis by Colliers.

However, that take-up was down from the 75-80 per cent rate over the past year, a sign that the availability of premium grade options was running out.

The headline vacancy rate also masks the fact that conditions were tightening at the top end, according to Colliers’ research head in Australia, Joanne Henderson.

“With no new supply replenishing the premium and high-end A-grade market, leasing activity is increasingly focused on A and B-grade stock.

“This trend is expected to persist due to the limited upcoming supply, particularly in markets like the Sydney and Brisbane CBDs, where premium options are scarce and minimal new supply is expected over the next 18 months.”

Sublease vacancy in the CBDs – which ballooned in response to the pandemic as businesses sought to reduce their real estate footprints – has decreased to 0.8 per cent, the lowest level since July 2020.

However, while the race for space at the top end is supporting investment into a new generation of towers – such as the 55 Pitt Street and the Chifley South developments in Sydney – the high overall vacancy rate remains a boon for occupiers, according to Kernel Property’s Holly Bailey and Steve Urwin, who act for tenants.

“There are a handful of strong-performing premium-grade assets in each market and, after that, it’s a tenant’s playground,” Bailey said.

“Melbourne is still struggling to pick up the pieces while supply additions are continuing. The Labor government’s promise to legislate WFH will only keep it in the doldrums.

“For tenants that want to be in the small Paris end of Collins Street, it’s a different story, and opportunities are limited.”