The property boom in this sector has years to run: Centuria

The logistics boom will deliver handsome returns to landlords for at least three more years as they lock in higher rents, according to $4 billion Centuria Industrial REIT.

CIP – as the trust is known by its ticker – upgraded its 2024 financial year earnings guidance by 20 basis points to 17.2¢ per unit as it collects strong rents from its sheds at infill markets. It has reaffirmed its distribution guidance of 16¢ per unit.

With that upbeat forecast, CIP shares closed at $3.35 – 4¢ higher, or up 1.2 per cent – its highest since February last year.

“With limited new supply within these infill markets, rental growth is expected to be prolonged, providing the opportunity for continued positive rental reversion,” said CIP fund manager Jesse Curtis, who heads the trust.

Mr Curtis said industrial tenants had been able to absorb the rental increases. On average, rent accounts for about 5 per cent of a tenant’s total expense base. As a result, CIP has not experienced any arrears in its portfolio and all tenants were “paying their rent on time every month”.

As a result of a 6 per cent like-for-like rise in net operating income from stronger rents, CIP’s interim operating earnings – or funds from operations, as they are called by REITs – remained stable at $54.1 million year-on-year despite $25.3 million in writedowns over the six months to December.

Following a similar pattern the previous year, the writedowns were primarily concentrated on the trust’s long WALE assets – Telstra data centre in Clayton in Melbourne’s south-east and an Arnott’s Biscuit factory in Virginia – which posted a $25.5 million writedown in total. Across both properties, the combined valuation fall was 3.6 per cent. The remainder of CIP’s 86-asset portfolio increased its value marginally by $200,000 on a like-for-like basis due to new leases and rental growth.

New leases on horizon

Mr Curtis said CIP’s improvements in rent performance would be prolonged as 41 per cent of leases in CIP’s portfolio were set to expire in the next 3½ years, which would allow the trust to achieve re-leasing spreads of 51 per cent.

CIP’s entire portfolio was currently under-rented by 30 per cent due to these leases, Mr Curtis said.

That forecast spread is significantly higher compared to the 30 per cent re-leasing spread posted throughout FY23, which was what drove the upgraded guidance. Re-leasing spreads are the difference between what a landlord charges on an expiring lease, and what they get on a new lease for the same asset.

Nevertheless, Mr Curtis said the industrial boom would moderate and the 30 per cent rental surge that occurred in 2022 and 2023 would slow.

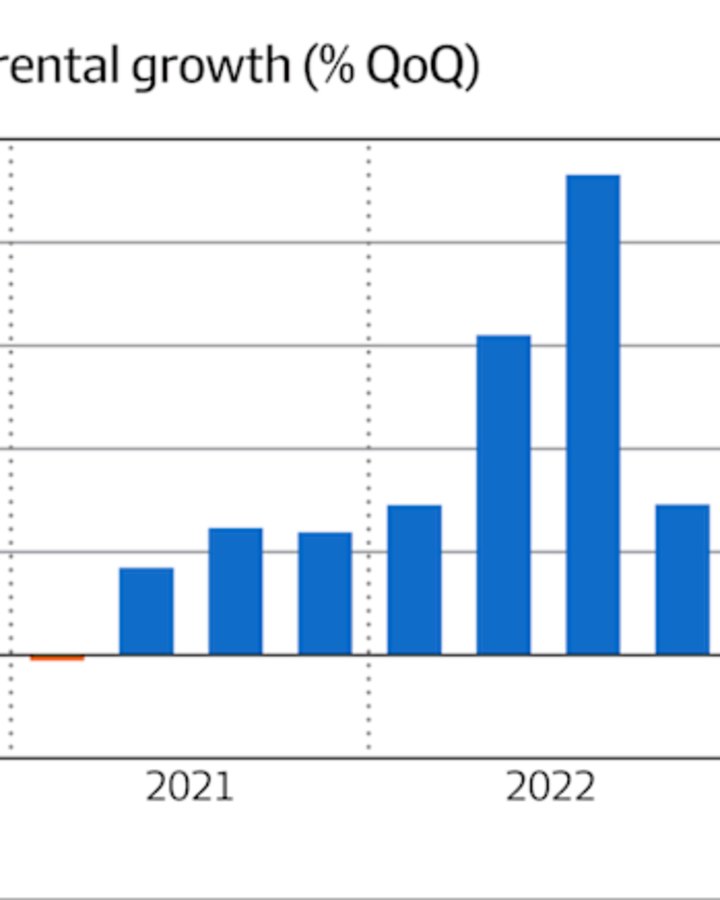

According to JLL, industrial demand remained resilient to the end of 2023 as rents in the three months to December increased 3.9 per cent quarter-on-quarter. While this was above average quarterly growth, it was down compared to the first three quarters of 2023.

For the entire 2023 year, industrial rents increased by 18.1 per cent year-on-year, which was the second-fastest pace recorded by the agency since it started tracking the series in 1989.

Plans to divest non-infill assets

Mr Curtis also confirmed to analysts on Wednesday that the REIT would continue to look for opportunities to divest its non-infill assets when citing his strong preference for infill-located assets. Currently, 17 per cent of CIP’s portfolio are non-infill locations.

“You can expect to continue to see us trimming the portfolio from a quality perspective,” he said.

Any divestments would help fund CIP’s optional $1 billion development pipeline, which was announced in its interim results. None of the development pipeline has been committed.

Moody’s Investors Service analyst Sean Williams called the results “credit positive” noting CIP would benefit from “strong rental growth an increase in like-for-like net operating income”.

UBS equities analyst Tom Bodor said re-leasing spreads had lifted “materially”, but the market would focus on how new supply dampens rental growth.