The few types of farming land holding ground while others slide

Farming land values will fall across the country as institutional capital pulls back and underlying profitability weakens, the founder of the $1 billion agricultural fund manager AAM, Garry Edwards, says, noting that only premium livestock and cropping assets will hold ground.

The market is increasingly split between high-quality assets that continue to attract investor interest and lower-tier holdings that face pricing pressure, says Garry Edwards, who in 2022 paid more than $50 million to acquire the 4053-hectare Bective Station near Tamworth.

“There’s a big divergence in the market,” Edwards said. “Large, commercial-scale properties continue to attract capital and hold value, but we are seeing downward pressure in smaller, less strategic holdings.”

Although global capital still found value in Australian farmland, Edwards warned that price gains would remain muted without a sustained increase in commodity prices.

“They’re taking long-term views, but returns will be modest,” he said. “We won’t see an increase in values until we get a sustained lift in underlying commodity prices.”

He was particularly bearish on dairy, pointing to a fall in milk prices over the past 18 months and the retreat of Chinese investors, many of whom had already quit the sector.

“We’ve seen a significant exit, especially among Chinese investors who had previously poured capital into the sector,” Edwards said. “Many of those farms have since been sold off.”

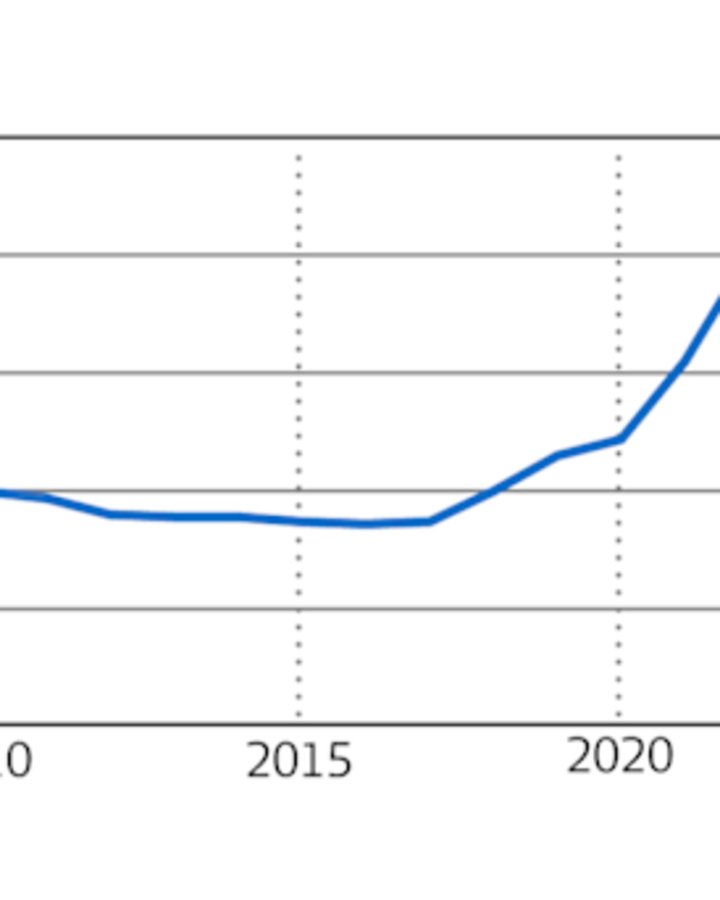

The sober forecast is reinforced by agricultural lender Rabobank, which in its latest annual farmland price outlook has flagged a sharp drop in offshore capital inflows and further pressure on dairy land values. Foreign investment in Australian farmland fell 38 per cent in FY2024 to $5.3 billion – the steepest annual percentage fall in 14 years.

“This is particularly notable in the dairy space where we are coming off a period of high profitability, with returns beginning to normalise,” said Rabobank analyst Paul Joules, the report’s author.

“This has likely taken the steam out of investment, and it could spell a return to more modest investment growth in the years to come.”

He said a rebound in foreign capital to the levels seen in 2022 and 2023 was unlikely under the current economic conditions, and described the pullback as part of a broader decline in corporate investment activity across the sector.

Against this backdrop, Rabobank forecasts a modest 3 per cent rise in farmland values in 2025 – up from last year’s 6 per cent decline, but a far cry from the explosive growth of the pandemic period, when median values rose 79 per cent between 2020 and 2023.

The report warned that the market had entered a slower phase, weighed down by persistently high input costs – especially fertilisers, urea and phosphate – and borrowing costs that remained elevated despite expectations of rate cuts this year.

“Rabobank does not expect to see the same heat in the market as witnessed between 2020 and 2023, as on-farm profit margins are expected to normalise,” it said.

The bank’s forecast is more subdued than its 5 per cent projection a year ago, which proved overly optimistic amid the broader downturn in land values last year.

Looking ahead, Rabobank predicts only moderate growth over the next five years, even if rates ease and commodity sentiment improves. However, it has signalled potential upside in commodity markets heading into 2025-26.

“For dairy and beef prices, market dynamics create room for upside in 2025, while for grains and oilseeds, declining global wheat stocks may provide price support,” Joules said.

Agriculture real estate agent Col Medway, who works at agency LAWD, said institutional investors continued to drive demand for large-scale rural properties, which meant the larger the deal, the easier it was to sell.

“There’s still a very strong appetite for quality beef properties in Queensland, and from the New England in NSW upwards, that is certainly strong. Equally, dryland cropping properties are also being sought after,” Medway said.

Institutional-grade assets remained resilient, buoyed by equity-funded buyers largely insulated from higher interest rates and supported by favourable currency conditions when bringing capital into Australia, he said.

Overall, Medway said, rural property values – including for smaller assets – had probably bottomed and were now set to enter a holding pattern.

“The history of rural land is it can move sideways for a long period of time and I think we’re going to be in one of those periods for some time,” he said.

“That’s because profit has to catch up to the lift, so I don’t think land values are going to continue to fall, but I don’t think there’s any great impetus for them to rise.”

Edwards, meanwhile, said AAM would prioritise investing in existing assets rather than pursuing new acquisitions due to the tough economic conditions.

“That’s not to say that if the right asset comes up, we won’t seek to acquire it, but we see a lot of opportunity and a lot of value in investing in our existing assets to create improved productivity,” he said.