Why this $140b industry super fund likes shopping malls so much

Kent Robbins, the property chief at $140 billion UniSuper, likes shopping. More specifically, he likes shopping centres so much that close to half the industry super fund giant’s unlisted real estate portfolio is invested in Australian malls.

What’s more, unlike some of its big peers – such as AustralianSuper, Aware Super and Hesta – the entirety of UniSuper’s $14.5 billion in commercial property is invested domestically.

Robbins’ commitment to retail is paying off. In Perth, the Karrinyup shopping centre – UniSuper owns it completely – has just hit $1 billion in annual sales, making it the first mall in the Western Australia to achieve that milestone, and joining a dozen or so other big centres nationally whose tenants clock up more than a billion dollars in sales each year.

That achievement more than doubles the $400 million turnover at Karrinyup previously, vindicating for UniSuper the decision to pursue an $800 million redevelopment at the mall.

UniSuper already has interests in some of the country’s biggest major malls, those posting billion-dollar turnovers, such as Pacific Fair on the Gold Coast and Macquarie Centre in Sydney.

Just last week, UniSuper’s exposure to the retail sector rose further still, as it took full control alongside Cbus Property of the Macquarie Centre, courtesy of a complex court battle that went against the previous owner of the stake, Dexus.

Behind UniSuper’s strong lean towards shopping malls is, as Robbins puts it, “simple maths”.

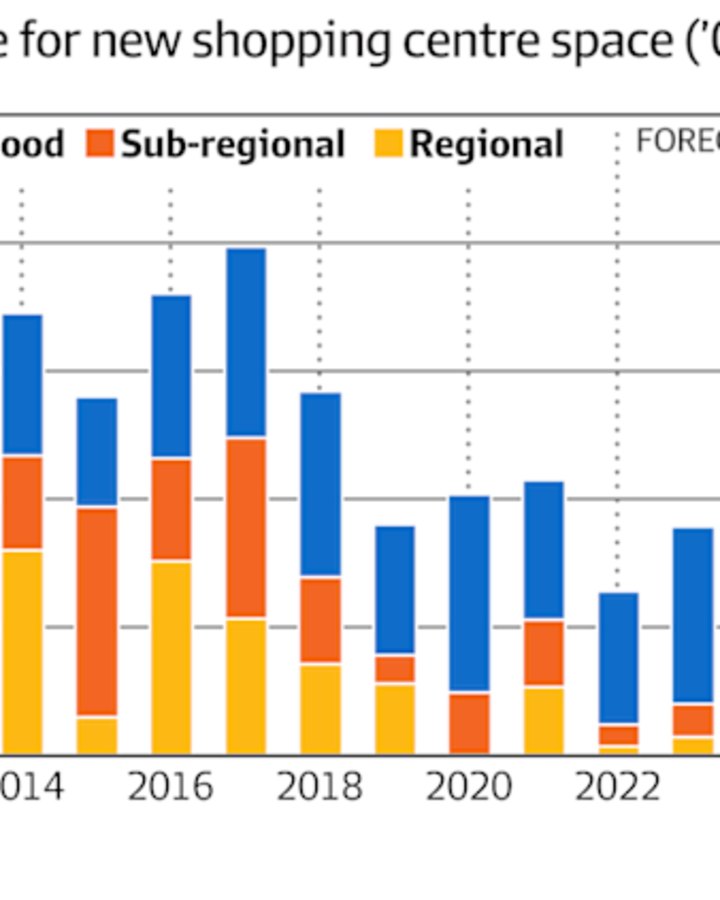

Australia is running out of mall space even as its population keeps growing. High construction costs mean it is effectively cheaper to acquire an existing shopping mall than to develop a new one, Robbins said.

“Why is no one building any super regional malls at the moment? You can buy them for 37 per cent less than what it would cost you to build them,” he told The Australian Financial Review.

“Everyone’s delaying or deferring their redevelopment of shopping centres because it’s not economic, and [at the same time] the population is still growing. Consumers still do a fair proportion of their consumption in bricks and mortar,” he said.

“So there’s a supply demand imbalance. [Retail] rents are rising. Income is good, there are very few incentives and income is growing. So for us, we just project out that total return and it looks very, very stable and looks really attractive.”

Of the $14.5 billion in UniSuper’s property book, some is invested in the big listed property companies, including shopping centre owners Scentre and Vicinity, along with the diversified investors and fund managers GPT, Charter Hall and Goodman. However, the majority, around $8.5 billion, is held in unlisted real estate: 45 per cent in retail, 30 per cent in industrial and 25 per cent in office.

“We look at each unit of population growth,” Robbins said.

“It needs more logistics. It needs housing and it needs retail. But not every single person making up the population growth needs an office. Not everyone’s employed, not everyone’s a white-collar employee. Everyone consumes, but not everyone consumes office space.”

“We’ve got high conviction on retail, but we’re not crazy, we’ve got high conviction on online retail [which requires warehouse space] as well. So we have a bet both ways. They [retail and logistics] are the two overweights.”

UniSuper has appointed GPT as its main investment manager, along with Richmond Bridge, which handles its industrial investments. The tie-up with GPT extends to an investment in its wholesale shopping centre fund, which invests in big malls such as Highpoint in Melbourne.

Overseeing all that at GPT is retail veteran Chris Barnett, who spent many years inside Westfield here and abroad before joining GPT.

“I’ve been in the industry for over 30 years and I haven’t seen the stars align as they’ve aligned today,” he said.

GPT has done some complex analysis to back up Robbins’ simple maths and arrived at the same conclusion: it’s too expensive for Australia to produce enough new mall space to keep up with its expanding population of shoppers.

On GPT’s estimates, there will be a shortfall in underlying demand for retail space – from major regional malls to smaller neighbourhood centres – of 1.1 million square metres by 2030.

As Barnett puts it, Australia added the equivalent of two super-regional malls each year for the past 30 years. Yet since COVID-19 and the inflation that followed, there’s been hardly any fresh development of major mall space.

“Moving forward, the next five to 10 years, we think it will be incredibly restricted.

“So you’ve got retailers being really profitable, enjoying high sales productivity. They are wanting to grow and they’ve got nowhere to go because there’s no new [mall] stock. We then create value by repurposing our existing centres.”