For the first time in four years, more workplace space was occupied in the last quarter in all the major central business districts than was left vacant, in a sign that the nation’s battered office market is turning the corner.

The green shoots are emerging most strongly in Sydney, where demand for space increased rents in the best buildings by 9.1 per cent in the past financial year, according to JLL.

The recovery is underpinning the case for a new generation of landmark office buildings in Sydney, such as Mirvac’s 55 Pitt Street – soon to be home to a dozen or so top law firms – and Charter Hall’s new Chifley tower.

It is also spurring renewed interest in opportunities such as the Halo tower, a 55-storey hybrid timber building proposed for the corner of Hunter and Pitt near the new metro station, where Cbus Property is in talks to take over.

“The rental growth story is not uniform across the Sydney CBD office market,” said Tim O’Connor, JLL’s head of office leasing in Australia. “We are seeing higher rents for well-located assets that are in close proximity to public transport, with superior levels of amenity. Shrinking availability in the core, in particular, is accelerating this.”

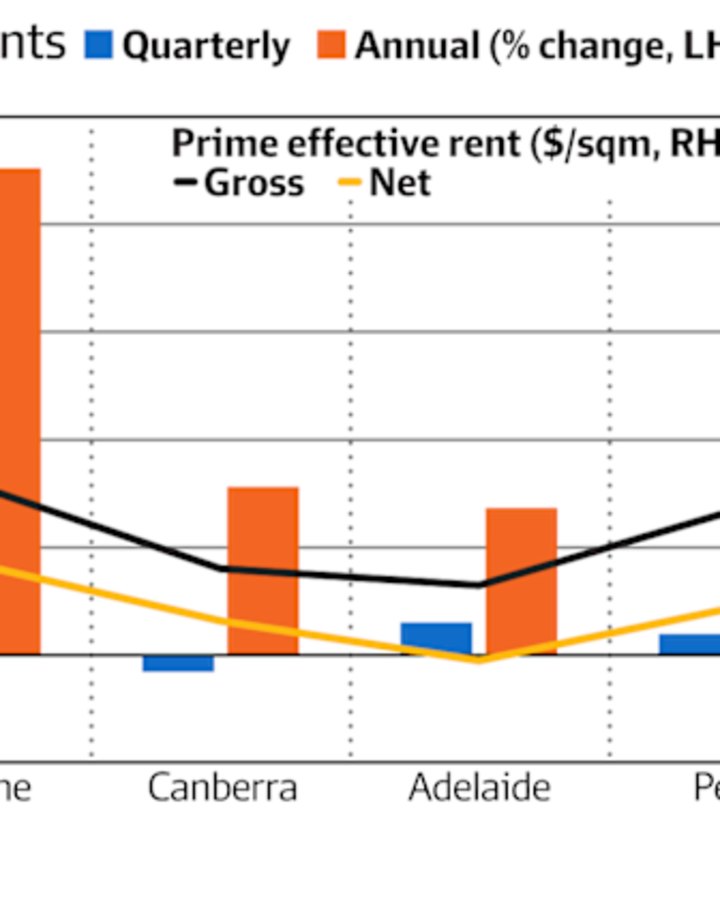

Sydney accounts for a large chunk of the fresh take-up of space, with 23,500 square metres overall in the second quarter of 2025. Nationally, the total take-up, described by the industry metric of net absorption, totalled 56,900 square metres.

As blue-chip bankers, lawyers and consultants race to secure their spots in a tight market, major investors are following, investing directly into major office buildings or committing their capital to Australian fund managers.

Big deals are in play, such as the proposed sale of Blackstone’s $1.4 billion stake in Grosvenor Place to fund manager Investa, backed by US investor BGO.

The JLL metric measures gross effective rents, a figure that incorporates both landlord incentives to tenants and all building outgoings. A separate figure for net effective rent excludes outgoings and focuses solely on the base rent after incentives.

The amount for rent collected after excluding incentives is crucial for landlords, fund managers and their investors and is factored into the business case for new investment.

Charter Hall managing director David Harrison said there is emerging evidence that effective rents are rising as incentives fall. Landlords are also limiting the cash component of incentives to less than 50 per cent, with the balance being rent rebates over lease terms, he said.

Harrison confirmed the rebound is most apparent in the CBDs’ most preferred precincts, such as Sydney’s core, Brisbane’s golden triangle and Melbourne’s east end. Modern towers are beating older assets in the early stage of the recovery, he said.

Underpinning the rebound is a return-to-work vibe that is increasing the space needed by existing renters, accompanied by tenants relocating from fringe markets into the CBD. As well, in Sydney especially, some stock is being taken out of the market as buildings are demolished or converted.

“There has been an inflection in both peak incentive levels and trough asset valuations, which is highly logical. As effective rents rise, one would expect valuations to rise,” Harrison said.

Fund manager Investa, led by Peter Menegazzo, is tapping into the recovery through its unlisted commercial property fund, which recorded its second consecutive quarter of positive returns, outperforming the annual benchmark by 3.1 per cent in the last financial year.

The fund manager has led a string of investment deals involving offshore capital into Sydney office blocks – Daibiru at 135 King Street, UOL and SingLand at 388 George Street, and BGO at 10-20 Bond Street – while leasing close to 100,000 square metres across its portfolio.

“This leasing momentum is translating into performance,” Menegazzo said. “With valuations below replacement cost and new supply constrained by elevated construction costs, vacancy is tightening, and effective rents are rising – a trend expected to continue.”

“The market is on an upward trajectory. Fundamentals are strengthening, leasing momentum is real, and investor confidence is returning with high-conviction capital already moving.”