‘Income up, rates down’. Tailwinds blow for property

In the past year, the Commonwealth Bank committed an additional $10.5 billion – well ahead of its 2024 commitment – to commercial property.

The CBA, which now has an exposure of $105.4 billion to the sector – including a modest exposure to residential development – wrote in its annual results presentation of its “well-secured portfolio” and “diversified growth” and stressed the “improving” market conditions.

The same market message was delivered by virtually every listed commercial property group reporting in the past month.

Income is growing, interest rates have turned to become a “tailwind”, valuations have stabilised, investors are looking to buy and, as the CBA demonstrates, even financiers are supportive.

Charter Hall chief executive David Harrison told his investors that with the “turning of the revaluation cycle”, the financial year 2025 was “clearly the inflection year”.

“Existing investors and new investors are seeing the same thing we are seeing: Australia screens as one of the best markets on a risk-return basis for core real estate,” says Harrison

Which raises a key question for the Financial Review Property Summit in Sydney next Monday and Tuesday. What happens now?

First, a look at the reports. On Monday, with most results in, UBS noted that around 68 per cent of the A-REIT results had led to upwards revision of earnings, with the average upgrade at 1.5 per cent.

Prices shifted even more dramatically than earnings – both up and down – in a trend that reflects the big rises and falls on the broader equity market.

In property, the big stock risers over the past month include Centuria Capital, up 39 per cent, Charter Hall Group (17 per cent), Stockland (14 per cent), Charter Hall Long Wale REIT (12 per cent), Charter Hall Retail REIT, (11 per cent), GPT Group (11 per cent) Aspen Group (10 per cent) and Scentre Group (9 per cent).

The big down movers have been DigiCo Infrastructure REIT, Centuria Office REIT and Goodman Group, Australia’s largest listed property group, now with a big focus on data centres.

Goodman, which topped $37 on the morning of its results has fallen away, dropping to around $34 on Wednesday.

Goodman forecast another 9 per cent growth in earnings in 2026 but UBS downgraded the stock to neutral due to a “less appealing valuation, slower-than-expected data centre development progress, and underwhelming operational metrics compared to high expectations”.

JP Morgan did lower its price target to $38.50 but still has an overweight rating with the group “well-placed to deliver low double-digit EPS growth over the medium term”.

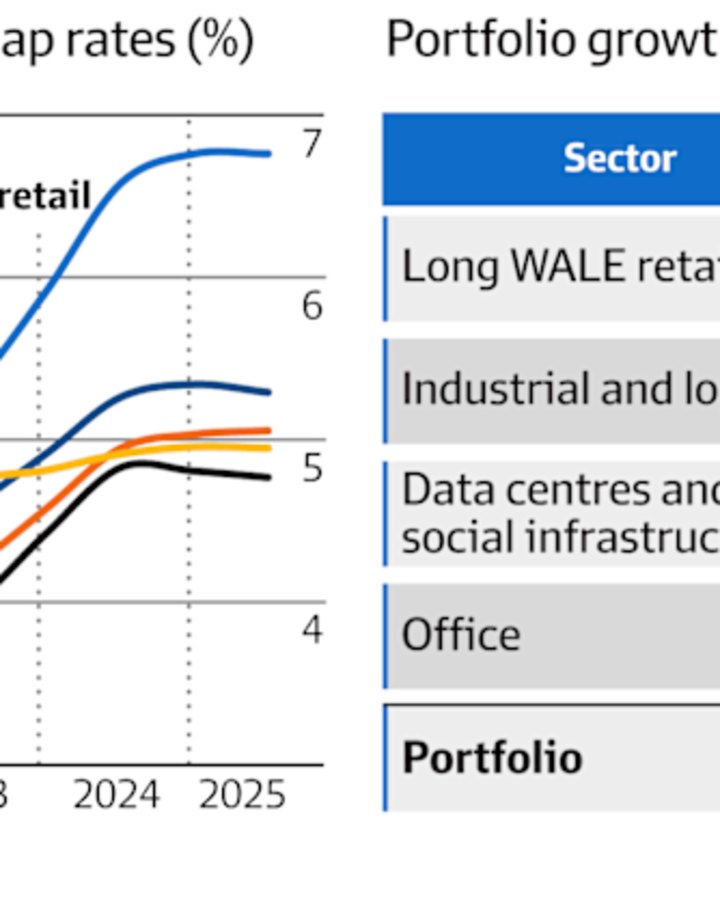

Today’s graphics, from the Charter Hall Long WALE REIT (CLW) portfolio, give a sense of how values have moved since COVID-19.

Capitalisation rates – akin to an investment yield applied to assets in the property sector – which tightened with interest rates from June 2020 to December 2022, have largely decompressed back to June 2020 levels, but because income has continued to rise the actual values are up strongly.

The increase is 35 per cent for long WALE (weighted average lease expiry) retail, 31 per cent for industrial and logistics and 19 per cent for data centres and social infrastructure.

The exception, of course, is office where continued cap rate expansion has offset income growth and left CLW’s office holdings worth 16 per cent less than in June 2020.

For offices in lesser positions or with vacancies the downturn would be wider. Abacus Group estimated that the fall in value since COVID is closer to 30 per cent.

Empty office space, either because of location or configuration, is still a drag on earnings for Dexus, Centuria Office and Abacus.

“If you are in the wrong part of town you are going to be a price taker,” said Dexus chief executive Ross Du Vernet.

Retail was the standout traditional sector in the latest round of results.

Scentre Group, with improved income – 29 of its 42 malls are full – and improved finance costs, has upped the forecast distribution for the second half of its financial year.

Vicinity Centres chief executive Peter Huddle said his portfolio was “essentially fully occupied”, and, as sales productivity had outpaced rents, so “headroom exists for substantial rental growth”.

Charter Hall Retail chief executive Ben Ellis spoke of “unbelievable investor demand for convenience retail”, which, when combined with rising income would see “valuations continue to grow”.

The industrial and logistics sector was less of a focus this year, as, with increased supply and reduced absolute growth in rents, the talk turned to the rental growth embedded in portfolios by the explosive demand of the post-COVID years.

So what is the outlook?

In very general terms, supply, which is a key determinant of property performance, remains constrained while the population continues to expand.

Construction cost inflation has normalised – both Mirvac and Lendlease noted the change – but the 40 per cent plus surge in costs since COVID makes all but the most ambitious projects uneconomic.

“It is still challenging on the basis of construction costs,” says Dexus’ Du Vernet. “Next phase of the cycle will be driven by fundamentals.”

Charter Hall’s Harrison has seen such cycles before. First comes the income growth, then cap rates tighten and valuations start to rise, and eventually income and valuations are surging together.

He also noted that after years of strong interest in alternative sectors – like health and living and data centres – his clients were reassessing the traditional sectors like retail, industrial and office.

Centuria Capital joint chief executive, John McBain, who has a new Centuria Port Adelaide Industrial Fund, predicted that 2026 would be “a more compelling real estate investment environment”.

Grant Berry, director and portfolio manager at SG Hiscock & Company, expects “selective acquisitions, potential capital raisings and some potential for M&A as the cycle progresses”.

But Black Swan events happen and the big themes don’t always play out as expected.

As HMC Capital chief executive David Di Pilla told his investors last month, “it may not be a linear journey”.