How many data centres Australia needs and where they will go

A race is on between Sydney and Melbourne as demand for data centres to support ballooning global growth in artificial intelligence, and rising demand for cloud computing, puts a rocket under the growing asset class in land-rich and well-connected Australia.

The NSW capital leads the race so far, accounting for 56 per cent of the $30 billion sector today, with Victoria’s capital at 30 per cent, commercial agency CBRE estimates.

At a time of lacklustre economic growth, political leaders have seized on the opportunity of what was until a few years ago seen as a niche sector.

“If you look at just one burgeoning industry – data centres – NSW is already leading Australia and is one of the leaders in the world,” state planning minister Paul Scully told the Financial Review Property Summit earlier this month.

“We have 90 data centres approved and another 20 under assessment, but we need to do more so the world knows NSW is investment ready.”

But the likely growth of 50 per cent over the next four years, which the commercial agency says will increase the sector’s value to $46 billion by 2029, will lift the southern state’s share to 33 per cent even as NSW stays about the same percentage, reflecting a growing divergence in what the two largest states offer investors and operators.

In Victoria, Danny Pearson, the Minister for Economic Growth and Jobs, says the state’s diminished manufacturing sector has left it with a plethora of well-located land, close to the city and already serviced with water and power, that could be repurposed for the growing sector.

“I love data centres,” he said last month. “Data centres are going to be to the 21st century what the rail lines were to the 19th century. I think we’ve got some natural competitive advantages and I want to see as many data centres as we can.”

Both states are developing systems to fast-track data centre planning proposal assessment.

In Victoria, the so-called Development Facilitation Program offers a pathway for data centre projects with a development cost of $20 million in metropolitan Melbourne and $10 million in regional Victoria.

NSW has created an Investment Delivery Authority which, when it opens to domestic and international investors this year, government sources say is expected to fast-track 30 major projects worth more than $1 billion each year, most of which will be data centres, by assessing them as state-significant developments.

Such is the demand for a digital backbone to the evolving global economy that both cities can benefit, says Craig Scroggie, the chief executive of ASX-listed developer and operator NextDC, which operates 17 data centres in Australia, New Zealand and Asia, and has facilities in Sydney and Melbourne.

“The status of Victoria and NSW is not a zero-sum game,” Scroggie says. “Both states can be hugely successful in a global sense in securing AI.”

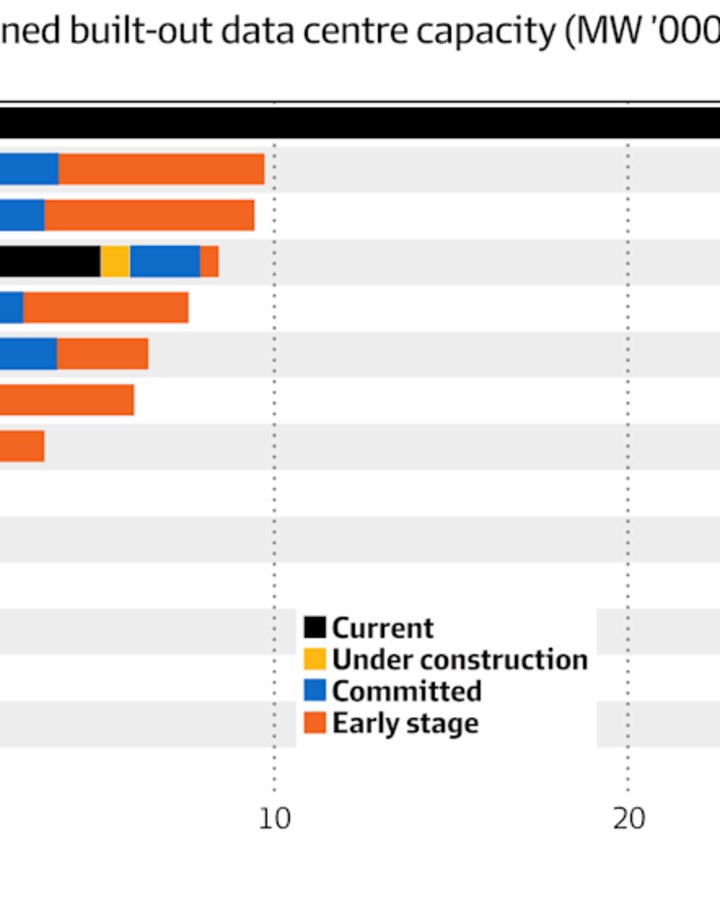

The opportunity is certainly global. A new report by CBRE says Australia’s current and planned data centre capacity of almost 10,000MW puts the country in third place after the US – a long way ahead with 30,000MW – but close behind India.

But demand is outstripping supply. CBRE estimates data centre demand of 2.5-3.5GW by 2028, meaning the country – with an estimated 1.8GW of capacity by then – will have a shortage of up to 1.7GW.

Data centre vacancy has tightened, with the time now taken to fully lease IT capacity falling from 40 months in 2020 to 13 months in 2024, the agency says.

Sydney and Melbourne are likely to diverge in what they can offer this evolving sector, says CBRE’s head of industrial logistics and data centre research for Australia, Sass Jalili.

“Sydney’s ability to expand is limited by land scarcity and grid connection delays, while Melbourne benefits from more available land but still faces infrastructure bottlenecks,” Jalili says.

“Both factors directly influence their capacity to develop as data centre hubs.”

Real estate considerations are key. Sydney’s scarcity of land and higher construction costs are pushing developments in the city towards smaller footprints and vertical assets. Melbourne, by contrast, has larger sites suited to campus-style developments that are more cost-efficient and scalable for investors, Jalili says.

Both cities also face challenges. Sydney’s biggest constraint is power access for new developments, while in Melbourne water is more of an issue, she says.

These hurdles are creating opportunities for smaller cities, Jalili says.

“Constraints in Sydney and Melbourne are accelerating diversification, with markets like Perth, Brisbane and Adelaide attracting new projects, broadening Australia’s data centre footprint and strengthening its overall investment appeal,” she says.

The market is also developing, with different operational models standing out for clients and operators.

Retail co-location, the smallest-scale use, is where enterprise users rent data centre capacity by the rack [of computers] for short periods of, typically, three to five years. Wholesale co-location is where larger tenants pay for the service by the cage or data hall on contracts of five to 10 years; and hyperscale is where large users, such as cloud operators, pay for a data hall or whole building to support their business.

Hyperscale centres will provide the bulk of demand for new facilities, prompting a wave of syndication or joint-capital investments, widening the pool of institutional capital in the sector, CBRE says.