‘Eyes wide open’: How to ride the private credit boom

Duncan Clubb, the national leader for business restructuring at global accounting and advisory firm BDO, has an increasing amount of work from non-bank lenders with problem loans to residential developers.

“We are seeing ongoing and sustained levels of inquiry from non-bank secured lenders with exposure to commercial real estate,” he says.

“Typically, the project is no longer viable or the sponsor (the developer) has no equity left. Increased capital costs are forcing lenders to take action.”

At the same time, non-bank lenders have taken a hit in high-profile property collapses, from John Adgemis’ Public Hospitality Group to Jean Nassif’s Top Place.

Yet the interest in private credit, including non-bank commercial real estate debt, has never been stronger.

In recent weeks Regal Partners and HMC Capital have spent in excess of $365 million buying key private credit operations Merricks Capital and Payton Capital respectively.

Today’s column will look at the paradox of pain and opportunity offered by private real estate credit, and then let two veterans of the industry provide a balanced assessment of the outlook.

Australia’s private real estate credit is a growing, $75 billion market, which currently accounts for about 16 per cent – compared to the banks’ 84 per cent – of the nation’s $447 billion in commercial real estate credit, according to Foresight Analytics.

It is diverse, from those who can raise $100 million in institutional capital to those who deal in thousands; not very transparent; and regulated as an investment product without the prudential oversight of the banks.

Australia’s Council of Financial Regulators – APRA, ASIC, the Reserve Bank and Treasury – did discuss the risks from lending to commercial real estate at their June meeting.

They concluded that the risks “remained constrained” due partly to the low exposures of the banks but agreed to monitor the “challenging conditions …particularly given the potential for stress in overseas markets to be transferred to domestic markets through foreign ownership and common sources of funding”.

The degree to which the regulators monitor the non-bank sector is hard to gauge. The sector takes investments, not deposits, and doesn’t gear funding as do the banks. But as the sector grows, so too will the question of oversight.

No question about the current stress in domestic residential development lending; it’s widespread. In fact, the resolution of the problems are fundamental to rebuilding affordable housing supply.

Extend and pretend a popular strategy

BDO’s Clubb says the non-banks increased their exposure to residential development as the banks reduced their appetite.

“These exposures were at the riskier end of the spectrum and have been more exposed to increased capital and construction costs,” he says.

Workouts vary. Extend and pretend seems a popular strategy.

At the same time, lenders have clearly encouraged many developers to attempt sale and exit. So far, fire sales seem very limited.

Widespread distressed selling, as happened in previous cycles, would rebase development site prices and be a catalyst to a construction revival.

“Some lenders have a preference to hold on with a view to market conditions improving, others are motivated to proactively address issues as they arise,” says Clubb.

MA Financial’s managing director, asset management, Cathy Houston, says few bank or non-bank residential development loan portfolios would not have defaults.

But default does not mean loss. Senior (first mortgage) holders can control the recovery process and be fully repaid.

“I expect there are a lot of lenders with losses on mezzanine loans, particularly development loans,” Houston says.

“I don’t think the number of defaults is going to grow materially from where they are now. Almost all construction loans have been extended and new construction loans are being written with more realistic labour expectations.”

‘Appealing and nerve-wracking’

The attitude of non-bank lenders is also important to broader commercial real estate, particularly in sectors where values have weakened.

“The non-bank lending sector is having a huge impact on the more stable nature of the current commercial property landscape,” wrote Wizel Property Group’s Mark Wizel in the May edition of Bricks and Mortar.

“The lack of visibility provided to the market by the players within the sector make it both appealing and nerve-wracking depending on which side of the fence one is playing.”

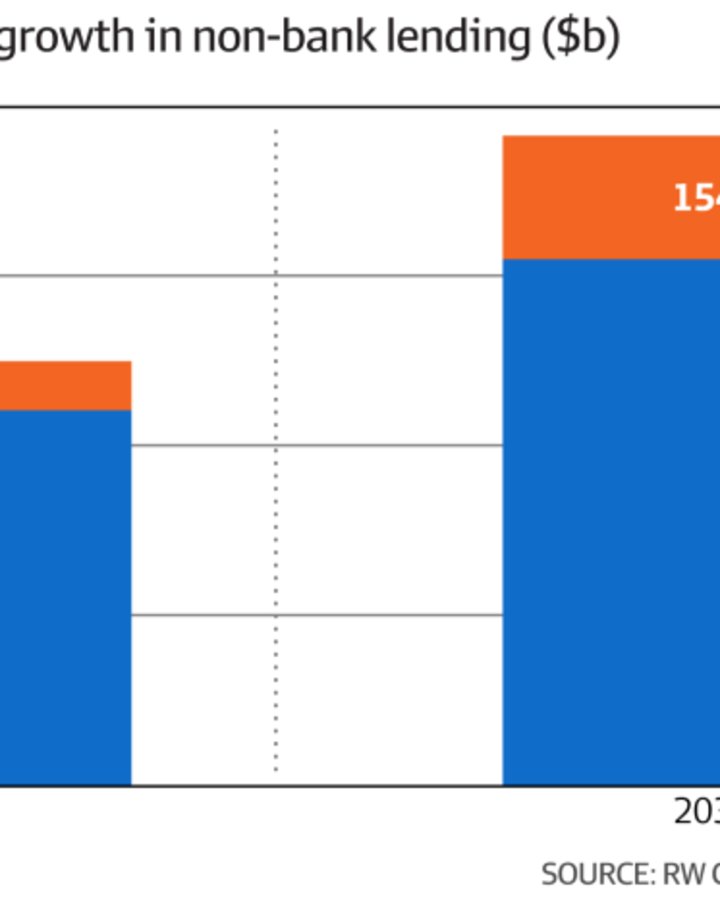

Nevertheless, all expect the sector to grow, in fact near double, to $146 billion and 22.7 per cent of the total CRE lending by 2028, according to Foresight Analytics.

Craig Schloeffel, the head of investment at Payton Capital, which commissioned the analysis, told my colleague Larry Schlesinger that the forecast was “quite conservative”.

“Non-banks make up 50 per cent of the commercial debt market in the US, so we are four to five years behind,” he said.

Increasing prudential restrictions on the banks, and a growing appetite from high-net-worth families for the risk-adjusted returns in private capital are key drivers.

A new report from Ray White’s RW Capital – which forecasts non-bank lending to rise to $154 billion by 2034 – summarises the financial attraction.

“Real estate private credit is gaining a larger market share of investment capital as investors seek a defensive source of yield and look to diversify away from real estate equity, while achieving strong, consistent, risk-adjusted returns that are secured and have strong, downside protection features,” says RWC head of institutional capital and research Luke Dixon.

“The defensive nature of private debt in the overall real estate stack offers enhanced safety, while the floating rate nature of returns provides a positive hedge against inflation.”

‘All of us need to be eyes wide open and alert’

Andrew Schwartz, the managing director of Qualitas – an alternative investment manager specialising in real estate credit and a leader in the sector with over $8 billion in funds under management – is a veteran of real estate credit.

”I am not seeing a sharp rise in bad loans, and I am looking for it because we are looking for debt recapitalisations,” he says. “I see one or two a month, not systemic or widespread.”

But he warns that interest rates have risen substantially, and the economy is slowing as the Reserve Bank addresses inflation.

“I have been doing this for 40 years and this would be the first cycle that could see an increase in rates and no increase in bad loans,” Schwartz says.

“All of us need to be eyes wide open and alert. It is real estate and it is credit. Let’s not misprice the risks.”

Michael Wood, chief executive of Madigan Capital, a specialist, institution-only commercial real estate debt manager, is also a veteran advocate for the sector.

“For investors into real estate debt the challenge is to differentiate between manager skill in identifying underwriting and pricing risk and those that have simply ridden the economic wave underpinned by a period of growth and low interest rates,” he says.

“The past decade or more in Australia has been an exceptionally good period to be a debt investor, but with the impact of a slower economy driven in part by higher interest rates it is inevitable that this will provide headwinds for many borrowers with consequential borrower defaults.”

Like all in the sector, he can see the “headwinds” in the development sector and “commodity” residential projects.

“Inevitably, in any industry where you see lots of new entrants there is the increased potential for mispricing risk,” he says.

“Managers with deep experience in asset management through market cycles and notably managing distressed loans are critical to preserving capital.”