Everyone wants to be a fund manager. But can they?

Lendlease chief executive Tony Lombardo has proved adept at exiting unwanted operations. Now he must rescue a business he wants to keep.

His flagship Australian funds management operation – the three Australia Prime Property Funds and the $10.6 billion of office towers, shopping centres and logistics facilities they control – is slipping away.

Nothing is formal yet. But several key institutional investors are working up a proposal to move the management to rival property fund manager Mirvac and all the parties – Lendlease, its rivals, and the independent directors of the funds – are appointing investment bankers, spin doctors, and lawyers for the tussle to come.

The battle puts a spotlight on the huge global business of property funds management.

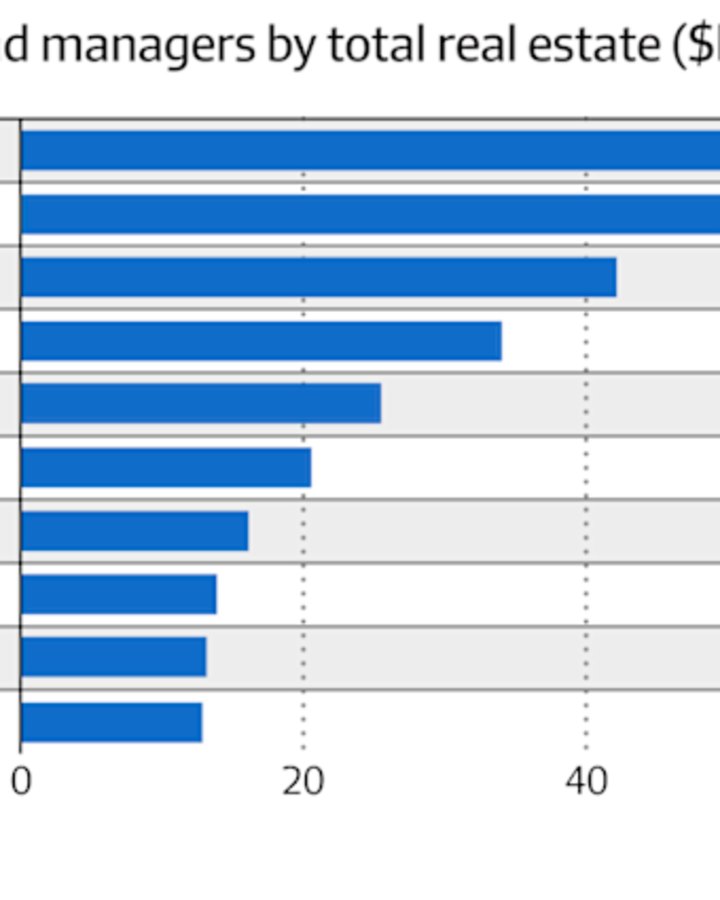

Global real estate assets under management totalled $US3.8 trillion ($5.8 trillion) in 2024 with the 10 largest fund managers, led by Blackstone, Brookfield and Prologis, controlling over half the market according to the latest Fund Manager Survey 2025 released in June by the Asia Association for Investors in Non-Listed Vehicles (ANREV).

ANREV estimates Australian groups have over $A330 billion in real estate funds under management – up 18 per cent over 2024 – with Charter Hall a clear, and growing, number one, and Lendlease number two because of its global funds management operations.

Curiously, neither those numbers, nor the accompanying ANREV league table, includes Goodman Group, which has over $70 billion in external assets under management.

Cash cows and pools

Everyone, or so it seems, wants to be a fund manager. It’s a capital-light strategy that delivers control and returns without weighing down balance sheets.

Fund performance over the past decade has been pretty anaemic, given the downturns in both office and retail sectors, but on some analysis global institutions are now underweight real estate.

“With asset performance in the Australian market showing signs of recovery, and given Australia’s reputation as a mature, transparent, and well-regulated institutional real estate market, we expect continued interest from both domestic and institutional investors”, said the chief executive of ANREV, Chris Hasse.

However, the nature of real estate funds management is changing, particularly for the so-called pooled funds, which, like the APPF vehicles, bring together a range of large and not-so-large institutions.

The big institutions want more control, more liquidity, and a manager fully committed to their interests. It is, after all, their money.

In particular, they don’t want to be treated as cash cows for their managers, or seen as just a number in a corporate balance sheet, or have their fund bought and sold to deliver cash to the manager and nothing to the investor.

The break-up of the AMP unlisted property portfolio, sparked – not unlike Lendlease’s current predicament – by corporate issues external to the funds, underscored the point.

AMP agreed to sell the real estate funds management portfolio to Dexus only to be rebuked by their investors who took their funds to Mirvac and GPT.

Earlier this year Macquarie Equity Research took a hard look at the sector in a report, A-REIT Funds Management, based on an ANREV survey of institutional real estate investors.

The survey showed that large wholesale investors have a clear preference for more control and increased liquidity.

“When weighted by assets under management, 50 per cent of ANREV survey respondents want to decrease exposure to pooled funds,” reported Macquarie Equity Research.

“Pooled funds still have a place and investors will support funds with a compelling investment proposition,” noted the report.

Nevertheless, Macquarie’s analysts concluded that “wholesale pooled fund redemptions present earnings risk” for Dexus, Mirvac, GPT, Charter Hall, and Lendlease.

Redemption story

Redemptions – how often to provide them, how much to pay out, how long is the payout queue, and how to fund them – are a perpetual issue for unlisted fund investors and managers.

Lendlease, which has a redemption window opening for APPF Retail later this year, has faced discord over APPF redemptions in the past but now faces a more existential challenge.

It could lose the management of the funds altogether, and with it about 10 per cent of its global funds under management, and some 30 cents of corporate value.

For Lombardo, Lendlease’s Investment Management platform is a core pillar of the group’s future strategy and growth.

In the first half of 2025 financial year, funds under management increased by 3 per cent to $49.6 billion.

More recently, the group cemented its mandate to manage Sydney’s Aurora Place on behalf of the National Pension Service of South Korea, introduced two new Japanese institutions into the Moorfields Investment Partnership in London, and won a small mandate from Malaysia’s largest public sector pension fund to invest across Malaysia and Australia in sectors like logistics, build-to-rent, data centres, healthcare and education.

The loss of APPF, which has been a core part of Lendlease for over 30 years, would be a big setback to Lombardo’s funds management ambitions and the future of the company.

In fact, it is important enough for Lombardo himself to be out meeting investors and selling the story.

Fighting back

“Our flagship APPF series in Australia is outperforming its MSCI/Mercer benchmarks, given the quality of the underlying portfolios, the performance and our ability to unlock embedded value,” he says.

“With around $750m invested across the APPF Funds, Lendlease is strongly aligned with unitholders.”

Lombardo points to the fact that the company has been fund manager since 1989 and has proven itself through market cycles.

”We are committed to leveraging our deep sector expertise to continue to create value for the benefit of all unitholders,” he says.

“We’re listening to our investors, and focused on meeting their needs, including maintaining competitive fee structures and proposing market-leading enhancements to liquidity mechanisms.”

True enough. APPF Office has outperformed its Mercer/IPD benchmark on every period for one, three, five seven and 10 years.

And yes, Lendlease has already pre-emptively cut its fees, down below the average 42 basis points of Gross Asset Value.

The difficulty for Lombardo is that institutional property funds management is about more than ticking those boxes.

As AMP discovered, it is also about investment choices, communication and a sense of ownership for those participating in the funds.

The institutions looking for a new manager feel that in the past APPF has been run less for investors and more for Lendlease.

Lombardo’s challenge is to convince them that the future will be different.

Robert Harley is a former Financial Review property editor. He can be contacted at rob@rharley.com.au.